A global macro hedge fund is a type of hedge fund that builds its portfolio around top-down economic and political analysis, taking positions in currencies, bonds, equity indices, commodities and other instruments based on how the manager expects the world economy to move.

Rather than picking individual stocks on company fundamentals, macro managers trade themes: a shift in interest rates, a currency that looks mispriced, a commodity cycle, or a policy decision they expect to surprise the market. The strategy is best known for headline-grabbing trades - George Soros breaking the Bank of England in 1992 is the obvious example - but in practice it is a disciplined, research-heavy approach used by some of the largest and longest-running funds in the industry.

This article explains how global macro funds work, what they invest in, the main strategies managers use, the risks involved, and how they compare with other hedge fund styles. If you are scaling a fund of your own, you may also want to read our deep dive into hedge fund strategies for a wider view of the landscape.

What Are Macro Hedge Funds?

Macro hedge funds, often called global macro funds, are alternative investment vehicles that profit from large-scale economic and geopolitical movements rather than from company-specific events.

The term “macro” refers to macroeconomics — the study of inflation, growth, employment, monetary policy, fiscal policy and trade. Macro managers form a view on where these variables are heading and express that view through liquid instruments across multiple countries and asset classes.

In short:

That difference in lens shapes everything else — the data they consume, the instruments they trade, the way they size positions, and the risk profile their investors should expect.

How Macro Hedge Funds Work

A macro hedge fund builds a thesis from economic data, expresses it through a small number of high-conviction trades, sizes those trades using leverage and derivatives, and manages risk dynamically as conditions change.

The typical workflow looks like this:

1. Research and thesis. Analysts and portfolio managers track central bank policy, inflation prints, employment data, trade flows, and political developments. The output is a directional view — for example, that a central bank will cut rates faster than the market expects.

2. Trade construction. The view is translated into the cleanest possible trade. That might mean buying short-dated government bonds, selling the currency, or using interest rate swaps and options to define risk.

3. Sizing and leverage. Macro funds typically use leverage, meaning they take exposures larger than the capital they hold, often via futures, swaps and repo financing.

4. Risk management. Positions are monitored against stop-losses, scenario tests and stress models. Macro books can change quickly when a thesis is wrong.

5. Liquidity discipline. Because macro trades rely on speed, managers concentrate on highly liquid markets — G10 currencies, sovereign bonds, large equity indices, major commodities.

The role of infrastructure here is significant. Real-time risk analytics, multi-asset execution, and clean data are not optional for a macro manager. We have written more about this in our piece on the operational infrastructure behind hedge fund performance.

What Do Macro Hedge Funds Invest In?

Global macro funds trade across asset classes, geographies and instruments — but the common thread is liquidity, because positions need to be entered and exited at scale without moving the market against the manager.

Typical exposures include:

- Currencies (FX). G10 and emerging market currencies, traded via spot, forwards and options.

- Government bonds and rates. US Treasuries, Bunds, Gilts, JGBs, plus interest rate futures, swaps and swaptions.

- Equity indices. S&P 500, Euro Stoxx, Nikkei, FTSE — usually via futures rather than single names.

- Commodities. Oil, gold, industrial metals, agricultural products, mostly via futures.

- Credit indices. CDX and iTraxx for broad credit exposure.

- Digital assets. A growing minority of macro funds now express macro views through bitcoin and other digital assets, particularly when reasoning about debasement, real yields or geopolitical risk.

The mix changes constantly. A macro fund that was heavily long the US dollar one quarter may flip to short the next, depending on the thesis.

Common Macro Strategies

Within global macro, managers tend to fall into two camps - discretionary and systematic - and several recognisable sub-strategies sit underneath that split.

1. Discretionary Macro

A portfolio manager builds the thesis and decides each trade. Examples include Soros-style currency speculation or Druckenmiller-style cross-asset positioning. Performance depends heavily on the judgement of the lead manager.

2. Systematic Macro

Algorithms generate signals from price data, fundamentals or alternative datasets. Trend-following CTAs are the most common variant. Decisions are rules-based and execution is largely automated.

3. Currency (FX) Strategies

Concentrated on developed and emerging market currency pairs, often expressing views on rate differentials, terms of trade or political risk.

4. Rates Strategies

Position around the shape and level of yield curves, central bank decisions, and relative value between sovereigns. This is where many of the largest macro firms make most of their money.

5. Thematic Macro

Long-horizon positions built around structural themes: deglobalisation, the energy transition, demographic shifts, the rise of digital assets. Implementation can span equities, commodities and currencies.

Examples of Macro Hedge Funds

Some of the largest and most influential hedge funds in history are global macro funds — and most are based in either London or New York.

- Bridgewater Associates, founded in 1975 with headquarters in Westport, USA. Known fo being the world’s largest macro firm for much of its history; pioneered risk parity and the All Weather portfolio.

- Brevan Howard, founded in 2002 with headquarters in Jersey and London. Known for being a European macro heavyweight; particularly strong in interest rates and FX.

- Rokos Capital Management, founded in 2015 with headquarters in London. Founded by ex-Brevan Howard trader Chris Rokos; concentrated, high-conviction macro book.

- Caxton Associates, founded in 1983 with headquarters in London and New York. One of the original macro funds, founded by Bruce Kovner.

- Element Capital, founded in 2005 with headquarters in New York. Discretionary macro fund founded by Jeffrey Talpins, with a heavy quantitative overlay.

- Soros Fund Management, founded in 1969 with headquarters in New York. Now a family office; the original Quantum Fund made its name on the 1992 sterling trade.

Risks and Criticisms

Global macro is a high-conviction strategy. When the thesis is right it can produce outsized returns; when it is wrong, drawdowns can be sharp.

The main risks investors should weigh include:

- Concentration risk. Macro books are typically built around a small number of large positions, so a single bad call can move the year.

- Leverage risk. The use of derivatives and financing magnifies both gains and losses, and creates margin obligations that must be met regardless of conviction.

- Timing risk. Being right about an economic outcome does not guarantee being right about the timing. Markets can stay irrational longer than a leveraged book can stay solvent.

- Key-person risk. Discretionary macro firms in particular can be heavily dependent on the judgement of one or two senior decision-makers.

- Capacity risk. Macro returns can degrade as funds grow. Several of the largest macro managers have returned capital to investors to protect performance.

Critics also point out that macro performance has been uneven over the past decade, particularly during the long period of central-bank-suppressed volatility after 2008. The return of inflation, rate cycles and geopolitical risk has improved conditions, but the strategy remains episodic.

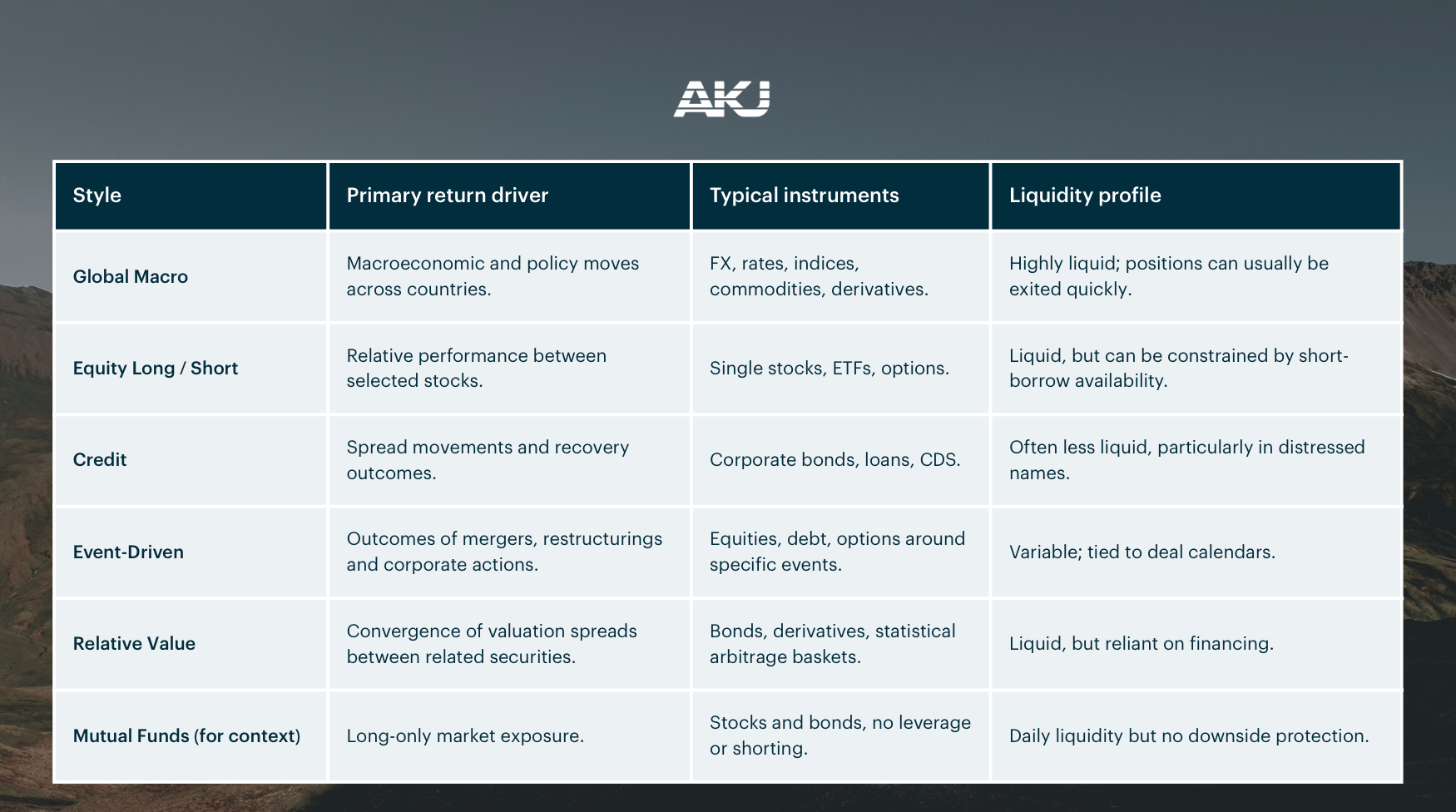

Global Macro vs Other Hedge Fund Strategies

Global macro sits alongside equity long/short, credit, event-driven and relative value as one of the core hedge fund disciplines - but it is structurally different from each of them.

The practical implication for allocators is that macro tends to behave differently from most other hedge fund styles, particularly in periods of stress. That low correlation is much of the reason institutional investors hold it.

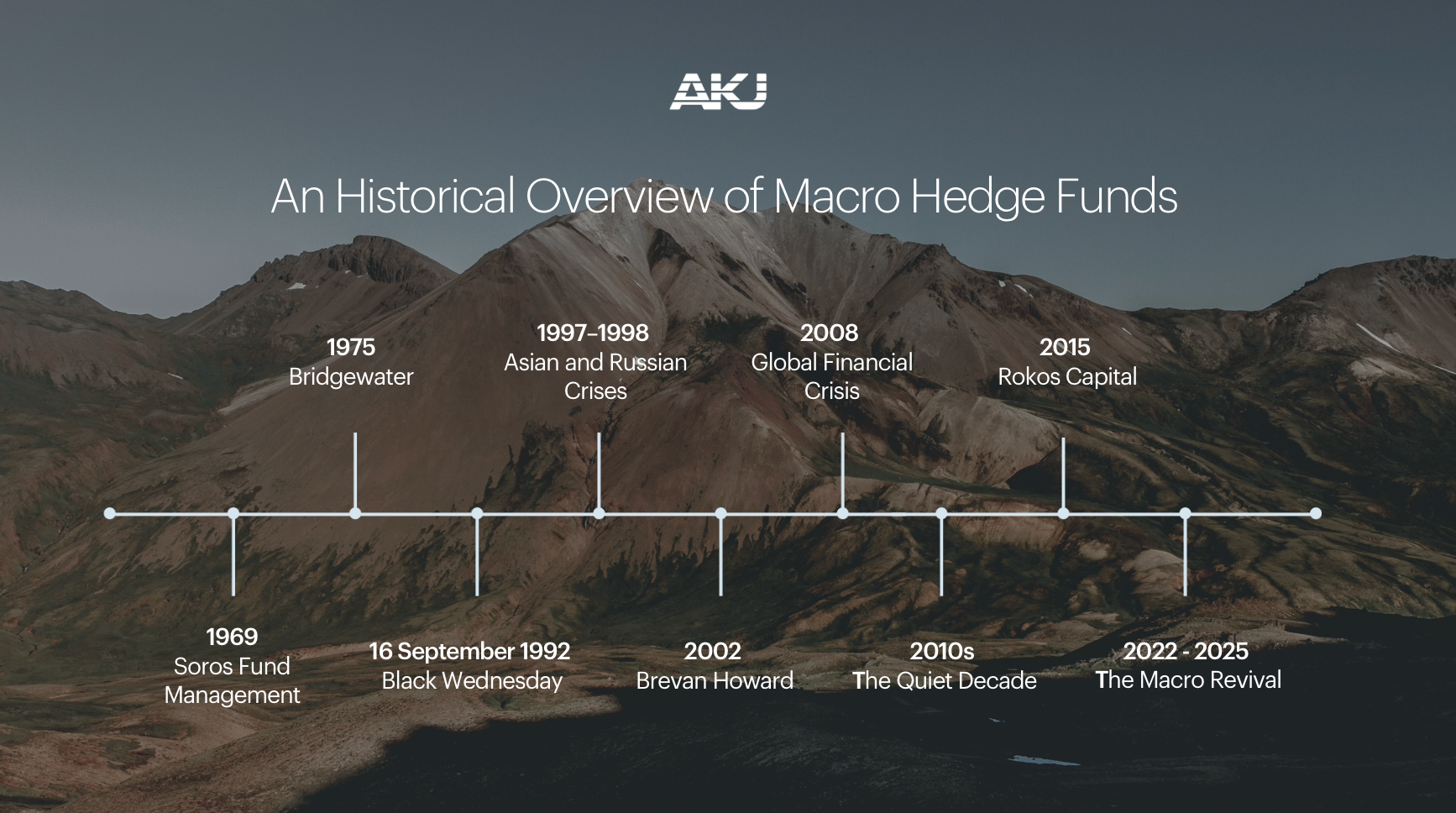

An Historical Overview of Macro Hedge Funds

The history of global macro is essentially the history of large policy and price dislocations — and of the managers who positioned themselves on the right side of them.

A short timeline of the events that shaped the strategy:

- 1969 – Soros Fund Management. George Soros launches what would become the Quantum Fund, applying his theory of reflexivity to currency and bond markets.

- 1975 – Bridgewater. Ray Dalio founds Bridgewater out of his apartment, eventually building the largest macro firm in the world.

- 16 September 1992 – Black Wednesday. Soros’s Quantum Fund makes a reported £1 billion shorting sterling as the UK is forced out of the European Exchange Rate Mechanism. The trade defines macro investing in the public imagination.

- 1997–98 – Asian and Russian crises. A second generation of macro managers profit from currency pegs collapsing across emerging markets, while LTCM’s failure shows the downside of leveraged convergence trades.

- 2002 – Brevan Howard. Alan Howard, Chris Rokos and others launch what becomes one of Europe’s flagship macro firms.

- 2008 – Global Financial Crisis. Several macro funds, including Bridgewater’s Pure Alpha, deliver strong returns by anticipating the credit unwind.

- 2010s – the quiet decade. Quantitative easing compresses volatility and most macro managers struggle. Brevan Howard halves in size, others close.

- 2015 – Rokos Capital. Chris Rokos launches his own firm, which goes on to be one of the standout performers of the next decade.

- 2022–2025 – the macro revival. Inflation, rate hikes, energy shocks and geopolitical conflict bring back the conditions macro funds need. Several of the largest discretionary funds post their best years on record and begin capping or returning capital to protect performance.

Summary

- Global macro hedge funds invest based on top-down economic and political analysis, not company fundamentals.

- They trade currencies, rates, indices, commodities and increasingly digital assets, almost always in highly liquid markets.

- The two main styles are discretionary and systematic, with several sub-strategies underneath each.

- Returns can be uneven and volatile, but macro tends to be uncorrelated with other hedge fund styles, which is why institutions allocate to it.

- The strategy has come back into form as inflation, rate cycles and geopolitical risk have returned to the front of investors’ minds.

If you are building or scaling a fund of any strategy — macro included — the operational and regulatory infrastructure matters as much as the investment thesis. Read more about the AKJ hedge fund platform, or learn more about us.

This article is for informational purposes only and does not constitute investment advice. Hedge funds involve significant risk and are typically available only to professional and institutional investors.

Read more:

- Deep dive into hedge fund strategies

- Hedge fund operations: the infrastructure behind performance

- AKJ hedge fund platform

- About AKJ