Cryptocurrency is a form of digital money that uses cryptography and a shared online ledger to prove who owns what, without needing a bank or government to keep track.

Instead of a central authority maintaining balances, cryptocurrencies run on networks of computers that collectively maintain and verify the record of transactions.

Cryptocurrency simply defined

A cryptocurrency is a digital asset you can send directly to another person over the internet. Ownership is tracked on a shared ledger, and transfers are secured using cryptography.

There is no physical coin or note. When you “own” crypto, you control cryptographic keys that allow you to move a balance recorded on a network’s ledger.

- Digital: it exists online only.

- Peer-to-peer: transfers can move between users without a bank as the record-keeper.

- Transparent rules: networks publish validation and supply rules in code.

- Always on: many crypto networks operate 24/7.

How it is different from traditional money

Traditional money (fiat currency) is issued by central banks and moves through regulated institutions such as commercial banks and payment processors.

Cryptocurrencies differ in a few practical ways:

- No single central bank sets issuance policy for most major cryptocurrencies, though protocol rules and governance processes can change over time.

- Transfers can settle on public networks rather than inside one bank’s internal ledger.

- Once confirmed on-chain, transfers are generally irreversibe; recovery typically requires the recipient’s cooperation.

Why does it exist?

Bitcoin was proposed in 2008, during the global financial crisis, by an anonymous figure writing as Satoshi Nakamoto. The idea was to create a form of money that does not rely on banks or governments to operate, and whose supply rules are fixed in code.

Since then, crypto’s use cases have expanded — from cross‑border value transfer to programmable applications.

How does cryptocurrency work?

Most cryptocurrencies combine three elements: a ledger (blockchain), a network of computers that verifies updates to that ledger, and cryptographic keys that prove ownership.

In plain terms, the network replaces tasks that banks normally perform: validating transfers and updating the shared record of who owns what.

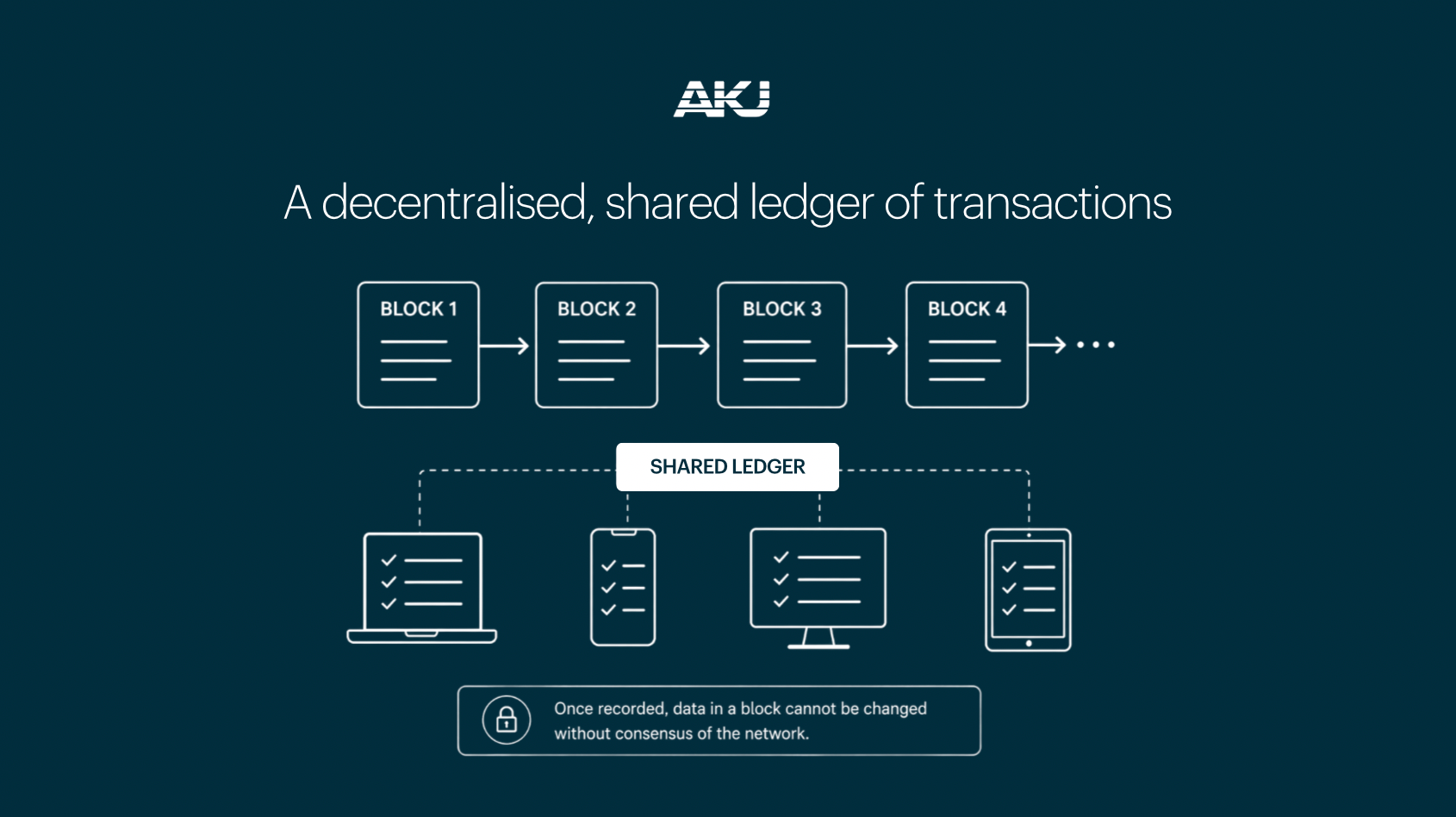

What is blockchain technology?

A blockchain is a digital record book. Transactions are grouped into “blocks” and added to a chain of previous blocks, creating an auditable history.

Each new block is linked to the one before it using cryptography, which makes retroactive changes extremely difficult without the change being obvious to the network.

Blockchain vs DLT vs cryptocurrency

Distributed ledger technology (DLT) is the broader category. It refers to systems where multiple participants share the same record of data.

Blockchain is one type of DLT that structures data into linked blocks. Cryptocurrency is the asset; blockchain (or DLT) is the underlying technology that enables it.

How transactions are verified

When you send cryptocurrency, your transaction is broadcast to the network. Miners or validators (depending on the system) verify that the transfer follows the rules and then add it to the ledger.

Because verification happens on the blockchain network, a bank is not required to confirm an on-chain transfer—though many people still use exchanges and banks for buying/selling crypto and moving money in and out of the crypto system.

What is staking in crypto?

In proof-of-stake networks, validators verify transactions and propose new blocks. Staking is the mechanism that requires validators (or people who delegate to them) to lock up crypto as collateral; if a validator breaks rules or goes offline, some networks can impose penalties (sometimes called “slashing”), while honest participation may earn rewards.

Staking is not risk-free: rewards are not guaranteed; your tokens may be locked or subject to waiting periods to unstake; validator or network issues can reduce returns; and the underlying asset price can move sharply. If you stake via a platform, you also take platform and operational risk.

Can you trust it?

Some major networks have long operating histories (for example, Bitcoin has operated since 2009), and many underlying cryptographic techniques are widely used across the internet. However, crypto systems can still fail in practice due to software bugs, smart-contract exploits, governance changes, or operational and custody weaknesses.

For most newcomers, the biggest risks are practical and operational: scams, weak account security, custody mistakes, platform failures and poorly designed projects.

Cryptocurrency vs traditional finance vs CBDCs

Most payments today are already digital — when you use a card or bank transfer, you are moving bank money inside regulated systems. Cryptocurrency differs because it can move on public networks without a bank acting as the record‑keeper.

Central bank digital currencies (CBDCs) are different again. A CBDC is a digital version of a nation’s fiat currency issued and backed by its central bank. Unlike most cryptocurrencies, CBDCs are centrally administered and designed to mirror fiat value.

A simple mental model: traditional finance focuses on regulated intermediaries; cryptocurrencies focus on open network verification; CBDCs modernise fiat rails while keeping the central bank in control.

A short history of cryptocurrency

Cryptocurrency is a young asset class, but it has already moved through several clear phases:

- 2008–09: Bitcoin is proposed and the network goes live.

- 2015: Ethereum launches, introducing smart contracts.

- 2017: ICO boom and rapid public attention.

- 2020–21: broader infrastructure and increased institutional participation.

- 2024: spot Bitcoin ETFs are approved in the U.S.; EU MiCA starts applying in stages (stablecoin rules from June 2024; broader rules from December 2024, with transition periods).

Examples of popular cryptocurrencies

A small number of projects account for most market attention. Common examples include:

- Bitcoin (BTC): the first and largest cryptocurrency by market value; often described as “digital gold” due to fixed supply rules.

- Ether (ETH): the native token of Ethereum; used to power transactions and applications.

- Stablecoins (e.g., USDC, USDT): designed to hold a steadier value, typically linked to the U.S. dollar.

- Other networks (e.g., Solana): built for fast transactions and application ecosystems.

Who uses cryptocurrency today?

Crypto users are not one group. The ecosystem includes everyday users, businesses, developers, traders, and institutions — each using crypto for different reasons.

Common real-world uses include:

- Payments and transfers (including cross-border).

- Trading and hedging in spot and derivatives markets.

- Stablecoin settlement as a bridge between bank money and crypto markets.

- Technology and applications built on programmable blockchains.

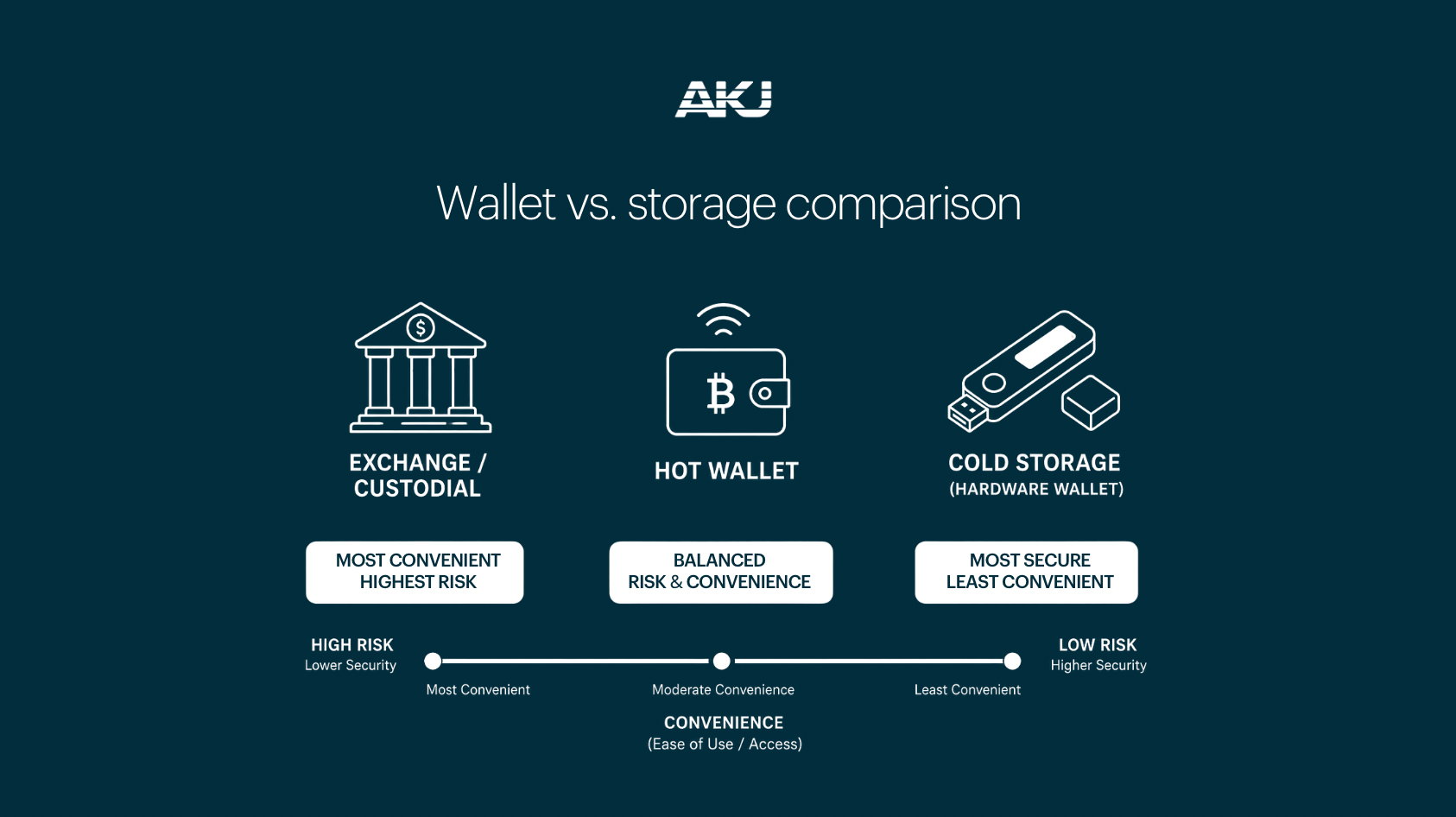

How to buy and store cryptocurrency safely

Most people buy cryptocurrency through an exchange or broker. Typically you create an account, complete identity checks, deposit fiat money, and place an order.

Where you store crypto after purchase matters. Security depends on how private keys are managed — and whether you or a third party controls them.

Practical security basics make an outsized difference: use strong, unique passwords, enable multi-factor authentication, verify URLs carefully, and treat unsolicited messages as suspicious by default.

What to look for when buying cryptocurrency

Many losses in crypto are linked to scams, platform failures, and poorly designed projects rather than failures of the underlying blockchain itself. A few checks go a long way:

- Check what legal and regulatory status (if any) applies to the service you plan to use in your jurisdiction.

- Understand custody: on-exchange holdings mean trusting the platform.

- Be sceptical of guaranteed returns or “risk-free” yields.

- Watch for impersonation and unsolicited messages.

How regulation impacts cryptocurrency markets

Regulation shapes how crypto services are offered, how client assets are held, and what consumer protections exist.

In the UK, certain crypto-asset businesses must register with the Financial Conduct Authority (FCA) for anti-money-laundering supervision, and marketing crypto to UK consumers is subject to the FCA’s financial promotions rules. In the EU, MiCA introduces a harmonised framework for crypto-asset issuers and crypto-asset service providers.

Key takeaway: rules and protections vary by jurisdiction and service type. Even where a firm is registered or supervised for certain obligations, crypto can still involve market, custody, and operational risks. This article is informational and not legal advice.

What are the risks and scams in cryptocurrency?

Crypto is a high-risk asset class. The main risks typically fall into a few buckets:

- Market risk: prices can move sharply.

- Counterparty risk: platforms can fail or restrict withdrawals.

- Custody risk: phishing, malware, and lost keys can mean permanent loss.

- Fraud risk: impersonation, fake support, and investment schemes.

- Regulatory risk: rules can change, affecting services and access.

Custody and storage options (quick comparison)

Commonly used terms in the crypto market

- Blockchain: Shared ledger that records transactions.

- Wallet: Tool that holds the keys needed to access crypto (hot = online; cold = offline).

- Exchange: Platform to buy/sell crypto (CEX holds assets; DEX lets you trade from your wallet).

- Token: Asset issued on an existing blockchain.

- Stablecoin: Crypto designed for price stability, often linked to fiat.

- Staking: Locking crypto to help secure a network, in exchange for rewards.

- Bull run: Sustained period of rising prices.

Summary

Cryptocurrency is digital money recorded on a shared ledger, typically a blockchain, without a central bank behind it.

The technology can be robust, but real-world outcomes depend on platforms, custody choices, and user security. If you are new to crypto, take time to understand how the technology works, what risks apply (including the possibility of loss), and what security steps you are responsible for.

Learn more

Learn more about our Digital Asset Fund Platform.

Read about the bull market in crypto.

See how crypto indicators work.

Read more about AKJ.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency is a high-risk asset class — values can fall as well as rise, and you may lose all of the money you invest. Crypto holdings are not protected by the Financial Services Compensation Scheme (FSCS).